Turning 65 is a major milestone, and for many people, it also marks the beginning of Medicare eligibility. While Medicare provides essential health coverage, it can also be confusing. Between enrollment periods, coverage options, and common misconceptions, many people are unsure what actually changes when they turn 65.

Understanding how Medicare works and what decisions need to be made can help you avoid costly mistakes and ensure your coverage fits your needs.

What Happens When You Turn 65?

When you turn 65, you become eligible for Medicare, the federal health insurance program for older adults and certain individuals with disabilities. Eligibility alone does not mean you are automatically enrolled in all parts of Medicare.

Some people are enrolled automatically, while others must take action to sign up. Missing key deadlines can result in late enrollment penalties or gaps in coverage, which is why early planning is important.

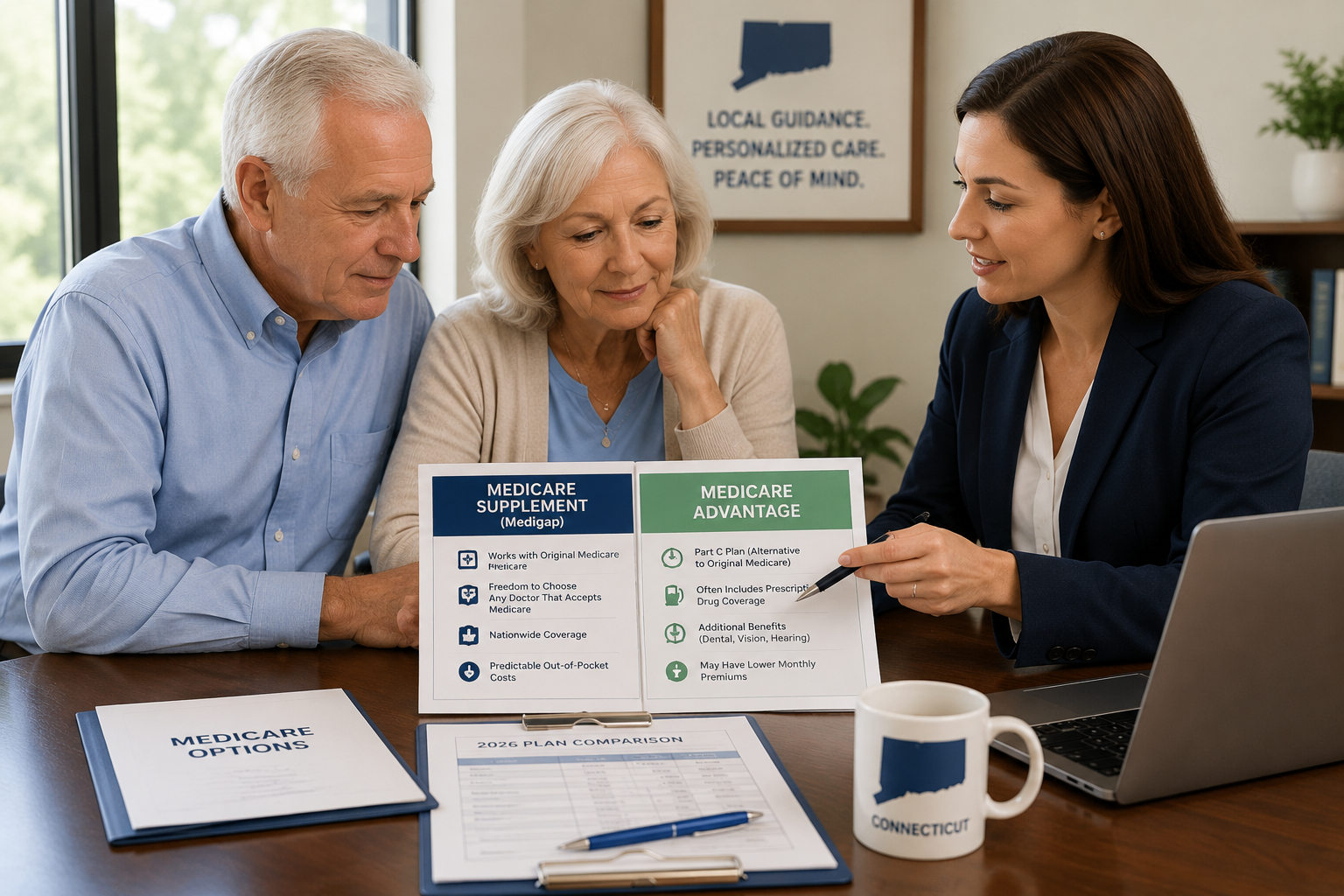

Understanding the Different Parts of Medicare

Medicare is divided into several parts, each covering different services:

- Part A covers hospital care and inpatient services

- Part B covers doctor visits, outpatient care, and preventive services

- Part C (Medicare Advantage) combines Parts A and B through private insurance plans

- Part D covers prescription drugs

Knowing how these parts work together is essential to choosing coverage that aligns with your healthcare needs and budget.

Are You Automatically Enrolled in Medicare?

Automatic enrollment typically applies if you are already receiving Social Security benefits before turning 65. In that case, you are usually enrolled in Medicare Parts A and B automatically.

If you are not receiving Social Security benefits, you’ll need to actively enroll during your Initial Enrollment Period, which begins three months before your 65th birthday and lasts seven months total. Missing this window can lead to penalties and delayed coverage.

Medicare and Employer Coverage: What You Should Know

If you’re still working at 65 and have health insurance through an employer, Medicare decisions can be more complex. Whether you should enroll immediately depends on factors such as employer size and how your current coverage coordinates with Medicare.

Some people delay enrollment without penalty, while others must enroll to avoid coverage issues. Reviewing your situation before making assumptions can help prevent unexpected costs.

Common Medicare Mistakes to Avoid

Many people make Medicare decisions based on incomplete or outdated information. Common mistakes include:

- Assuming Medicare covers everything

- Missing enrollment deadlines

- Choosing coverage based solely on monthly premiums

- Overlooking prescription drug coverage

Taking the time to understand your options can make a significant difference in both coverage quality and long-term costs.

Why Medicare Planning Matters

Medicare is not a one-size-fits-all program. Your health needs, prescriptions, travel habits, and financial goals all play a role in determining the right coverage strategy.

A thoughtful approach helps ensure:

- Access to preferred doctors

- Predictable healthcare costs

- Coverage that evolves as your needs change

Planning early gives you more choices and fewer surprises.

Get Guidance Before You Enroll

Medicare decisions can feel overwhelming, but you don’t have to navigate them alone. Having a clear understanding of what turning 65 really means and what steps to take next can help you move forward with confidence.

Ready to Talk Through Your Medicare Options?

If you’re approaching 65 or helping a loved one prepare for Medicare, the team at The Jones Group is here to help. We’ll walk you through your options, explain how Medicare works with your current coverage, and help you make informed decisions that fit your needs.